State of the PhilHealth fund: Claimed excess ignores reserve deficit and service gaps

The Department of Finance (DoF) claims that the Philippine Health Insurance Corp. (PhilHealth) has excess, idle funds. This claim ignores not only the staggering reserve deficit of PhilHealth, but also the yawning gap in healthcare financing. The DoF cites three bases for excess: 1.) a ballooning reserve fund, 2.) benefit claims lower than the subsidy for premium, and, 3.) the funds are no longer needed. Financial statements reveal that point No. 1 is contrary to law and insurance accounting standards. Legal and finance principles prove that point No. 2 is a ridiculous comparison. National health indicators debunk point No. 3 by showing a gap between the goal and reality.

The Universal Health Care Act mandated PhilHealth to set aside a Reserve Fund to cover short-term projected expenditures and an Investment Reserve Fund to cover liabilities beyond two years. The law caps the Reserve Fund at an equivalent to two years of projected expenses, and limits the use of excess funds to improving benefits, lowering contributions, or building the Investment Reserve Fund. No portion of the reserve fund or income thereof should go to the general fund. The Investment Reserve Fund is meant to cover long-term liabilities, but PhilHealth has not created one.

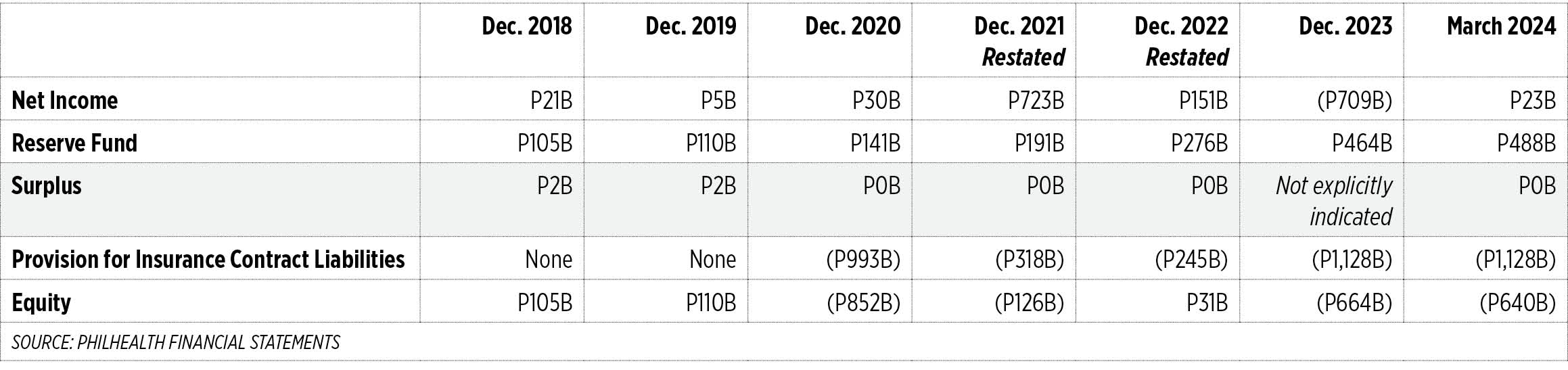

The DoF implied that the Reserve Fund has accumulated a huge balance, maybe enough to exceed its ceiling. Based on PhilHealth’s March 2024 financial statements, the Reserve Fund only amounted to P488 billion, which was still below the actuarial estimate of P560.55 billion. PhilHealth has yet to release updated financial statements and prove that there is an excess over the short-term Reserve Fund. Even the Commission on Audit (CoA) issued a qualified opinion on PhilHealth and questioned the accuracy of its actuarial valuation report.

The DoF stated that the fund transfer will not come from the reserve fund nor member contributions, but from the “unused” portion of government subsidies. But it’s not true that the reserve fund or member contributions will not be affected. The cash transfer reduced the asset side of the balance sheet, and would be matched by parallel changes on the liability and equity side: a decline in provision for insurance contract liabilities (ICL) and a decline in member’s equity. In determining the transfer amount, the government calculated the difference between the subsidy given (or premiums paid) for indirect contributors and actual benefit claims of indirect contributors. Government claimed that there were unused subsidies even if these subsidies were already spent on premium payments for indirect contributors. Government is seeking a refund of premia but expects insurance to remain enforced. This is against Sections 77 and 81 of the Amended Insurance Code, which states that “An insurer is entitled to payment of the premium as soon as the thing insured is exposed to the peril insured against” and “If a peril insured against has existed, and the insurer has been liable for any period, however short, the insured is not entitled to return of premiums, so far as that particular risk is concerned.”

Despite CoA’s comments on reserves accuracy, the DoF created a circular to implement the special provision of the General Appropriations Act calling for collection of government-owned and -controlled corporation (GOCC) funds in excess of reserves. The DoF appointed itself via circular as the calculator of reserve funds, which is a case of conflict of interest. The DoF cannot be both the arbiter of excess reserves and beneficiary of collected funds. The calculation of reserves is the job of the Actuary who ideally should be independent.

PhilHealth has been reporting zero surplus since 2020. According to PhilHealth, “Surplus represents accumulated profit of the Corporation after deducting transfers made to Reserve Fund.” It boggles the mind how PhilHealth can declare excess funds when it has zero surplus, and its capital (members’ equity) has been negative since 2020 when the Philippines adopted International Financial Reporting Standards for Insurance. These standards mandated setting aside reserve for insurance contract liabilities not only for current or two-year obligations but for the whole lifespan of members.

Technically, PhilHealth is already balance sheet insolvent. While it may have the cash to pay current liabilities, it has insufficient assets to fund long-term liabilities. For March 2024, liabilities (P1.252 trillion) were twice the assets (P612 billion), with Equity already negative at P640 billion. If PhilHealth won’t adjust policies or government won’t appropriate funds to plug reserve gaps, insolvency can lead to bankruptcy. Sadly, the false narrative of excess funds encourages proposals that worsen its insolvency, such as the arbitrary expansion of some benefit packages without the review and approval of technical bodies like the Health Technology Assessment Council (HTAC). It is still imperative, however, to expand and implement some important benefits like the Konsulta package or the primary care package.

Government contends that Section 29 (3), Article VI of the 1987 Constitution allows for the transfer of special fund to the general funds “if the purpose for which the special fund was created has been xxx fulfilled.” It adds that Section 11 of the 2024 General Appropriations Act (Budget) allows the reversion of funds to the National Treasury “when they are no longer necessary for the attainment of the purposes for which said funds were established.” The Philippines is still far from the goal of Universal Healthcare, of ensuring “that all Filipinos are guaranteed equitable access to quality and affordable healthcare goods and services, and protected against financial risk.” While mandatory coverage of all Filipinos brings PhilHealth membership coverage close to 100%, actual access and affordability of healthcare remain a challenge. The National Economic and Development Authority’s (NEDA) Sustainable Development Goals report shows that out-of-pocket spending as a percentage of total healthcare expenditures remained high at 39.9% (2020), while the percentage of births attended by a skilled health personnel was still below target at 84.4% (2017).

Every field has its bag of tricks. While some maneuvers may be acceptable, this transfer of PhilHealth funds glaringly violates legal, financial, and moral principles.

A former banker, Enrico P. Villanueva is now a senior lecturer for the University of the Philippines’ Department of Economics. He was a student of the late Carlito Añonuevo, co-founder of Action for Economic Reforms. This piece is written in memory of him.

{kind=link}