Ensuring debt sustainability through fiscal consolidation

The pre-pandemic period was often cited as one of the most successful episodes of fiscal consolidation in the Philippines. This was attributed to the government’s prudent fiscal policy which led to the steady reduction in the public debt-to-GDP ratio over the years.

Since 2020, the reserved fiscal buffer has helped Filipinos weather the pandemic storm and boosted the recovery of the Philippine economy through fiscal stimulus. Consequently, the public debt-to-GDP ratio has increased sharply. In response, the government plans to undertake fiscal consolidation to ensure public debt sustainability.

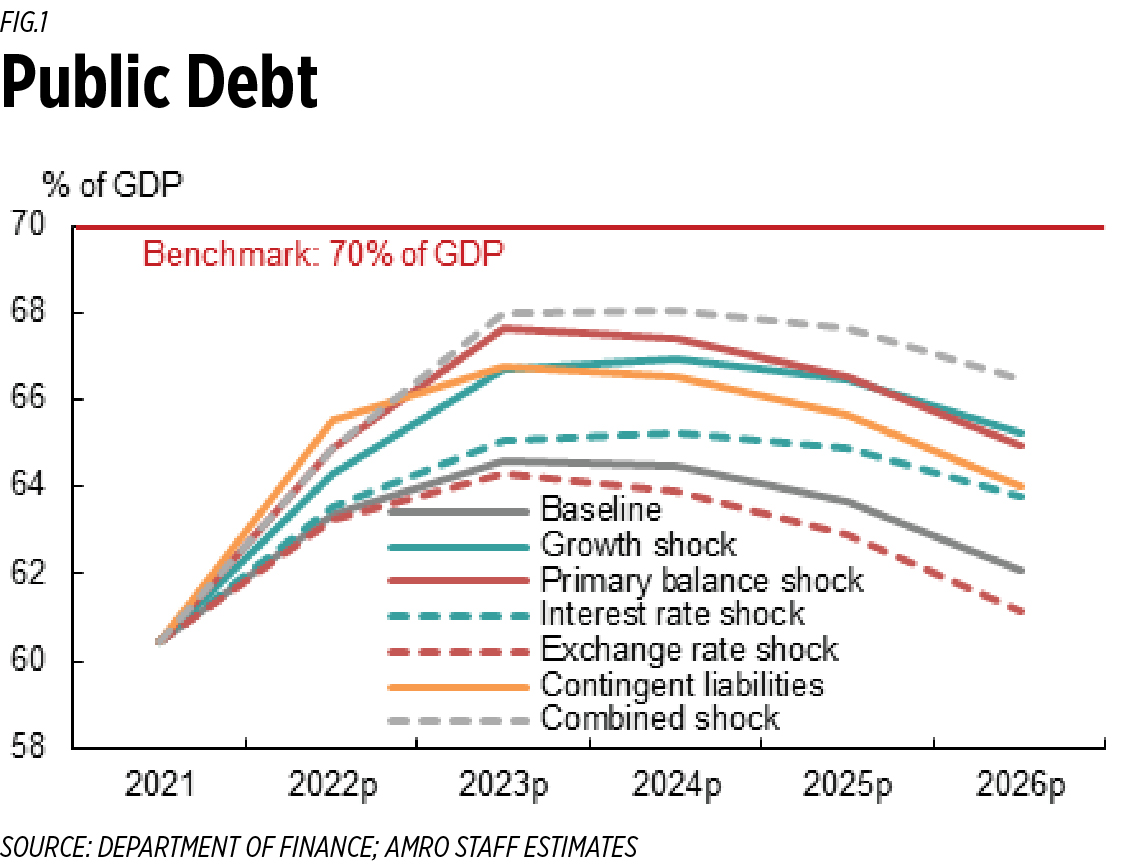

DEBT SUSTAINABILITY NOT AT RISKWith a strong economic recovery momentum and the government’s fiscal consolidation efforts, the Philippine debt-to-GDP ratio is expected to gradually decline in the medium term, after peaking at mid-60% in 2023 (Figure 1). AMRO’s stress test results under various shock scenarios reveal that the debt ratio remains below the threshold of 70%, as recommended by the International Monetary Fund (IMF) for emerging markets economies.

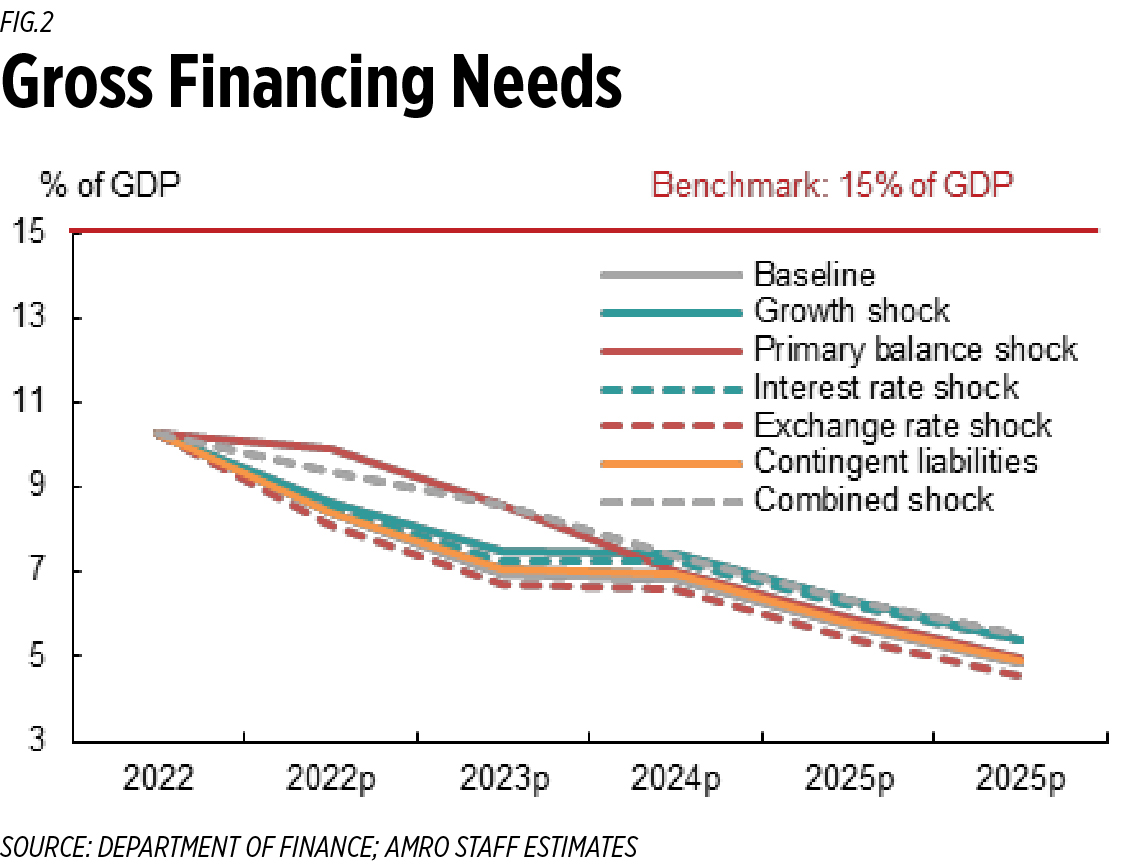

The baseline projection and stress tests for the gross financing needs, defined as the sum of fiscal deficit and amortization, also demonstrate low financing stress (Figure 2).

Moreover, market perception of the sovereign risk of the Philippines is regarded as low, as reflected in the stable Emerging Market Bond Index (EMBI) Global spread and Credit Default Swap (CDS) spread.

Notwithstanding the higher debt, the scarring from COVID-19, and the headwinds from the ongoing war in Ukraine, the Philippines has also succeeded in maintaining the investment grade of sovereign credit ratings by major credit agencies.

Furthermore, the debt profile of the Philippines has been broadly sound. External financing requirements stayed low, attributable to the stable amortization schedule of external public and private debt. The share of external debt has declined to 30%, mostly in the long maturity and with 44% in concessional terms, implying low liquidity risk arising from sudden shifts in the foreign investors’ risk appetite. The contribution of short-term debt is only 6.8%, making it less susceptible to rollover risk.

Overall, the risk of public debt sustainability in the Philippines is assessed to be low in all aspects — solvency, liquidity, and debt profile vulnerability.

ACCELERATE FISCAL CONSOLIDATION WITH A CREDIBLE PLANGiven the economic growth momentum may be moderated under high uncertainty, the government’s fiscal consolidation plan to gradually reduce fiscal deficit is deemed reasonable. In view of the concerns over the narrowed fiscal policy space and the limited buffers to address unforeseen future shocks, the pace of fiscal consolidation should be accelerated once private-sector growth becomes self-sustaining.

While unwinding the COVID-related spending, the government needs to continue strengthening revenue-enhancing measures; broadening the tax base, especially for VAT, and improving the efficiency of tax administration, including the digitalization of tax and customs duty collection. Raising excise tax rates and introducing new taxes on digital services could also be considered.

The government should also ensure the credibility of the fiscal consolidation plan.

The public debt-to-GDP ratio is projected based on the underlying macroeconomic forecasts and fiscal plans. Realistic macroeconomic forecasts and feasible fiscal plans are critical in setting achievable public debt-to-GDP ratio targets in the process of fiscal consolidation. Any significant errors in government debt forecast may hamper the credibility of fiscal plans and cause market sentiment to falter.

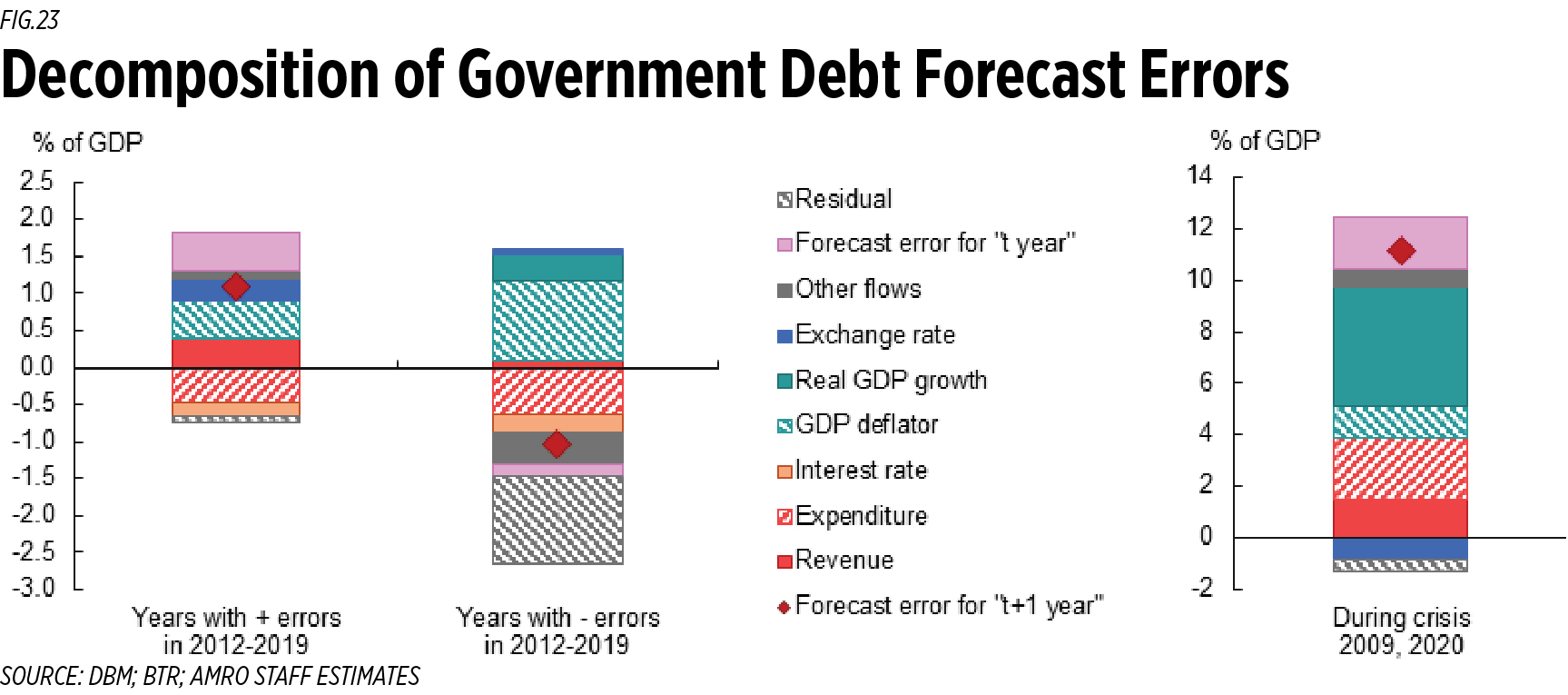

AMRO assessed the public debt forecast errors and identified the sources of errors in the Philippines by using the forecasts of official budget documents from 2009 to 2021 (Figure 3). It revealed that the forecast error in debt-to-GDP ratio projections was not insignificant. In particular, the GDP deflator inflation has been consistently over-forecasted, while the revenue shortfall and the expenditure underspending have been observed for many years.

During the 2009 Global Financial Crisis and the onset of the COVID-19 pandemic in 2020, the collapse in real GDP growth has been the major source of forecast error. The results suggest there is room to improve the macroeconomic forecasts and enhance revenue collection and expenditure disbursement.

To conclude, strong fiscal prudence over the past decade has enabled the Philippines to maintain debt sustainability despite the pandemic. Today, the government has kicked off another round of fiscal consolidation efforts to restore the shrunken fiscal buffer. In its journey ahead, establishing a credible plan based on realistic medium-term macroeconomic projections, and accelerating its implementation, depending on the economic developments, are necessary to ensure success.

Dr. Byunghoon Nam is Senior Economist with the ASEAN+3 Macroeconomic Research Office (AMRO).

![Photo of [HED] CloudSwyft deploys virtual lab in more schools](https://redstateinvestings.com/wp-content/uploads/2020/01/Screenshot-2019-03-20-at-09.24.29.png)

{kind=link}

{kind=link}

{kind=link}