Exiting the FATF grey list and getting credit ratings to ‘A’

Last week, on Feb. 21, the Philippines was taken off the Financial Action Task Force’s (FATF) grey list. That is good. The FATF is the global anti-money laundering watchdog, and the Philippines has been on the FATF grey list since June 2021.

Department of Finance (DoF) Secretary Ralph G. Recto is correct in his exuberance saying that “This is a landmark achievement of the Marcos Jr. administration. It’s a seal of good housekeeping that strengthens public confidence in our financial system. This will directly benefit our remitting overseas Filipino workers, businesses, and the Filipino people… we will attract more foreign direct investments and expand more trade partnerships that will help accelerate economic growth. With this momentum, our next goal is clear — a credit rating upgrade within the Marcos Jr. Administration.”

The DoF is a member of the National Anti-Money Laundering (AML) Coordinating Committee (NACC), Counter-Terrorism Financing (CTF), Counter-Proliferation Financing (CPF) — the inter-agency body responsible for overseeing the National AML/CTF/CPF Strategy (NACS) and guiding its implementation across relevant agencies.

On this development, see these related reports in BusinessWorld: “Investor sentiment likely to improve as Philippines is removed from ‘gray list,’” by Luisa Maria Jacinta C. Jocson (Feb. 24), and “Philippines exits global watchdog’s dirty money ‘gray list’” (Feb. 23).

The prevalence of Philippine Offshore Gaming Operators (POGO) in recent years was the main factor for the Philippines’ inclusion in the grey list. The POGOs were involved in lots of money laundering activities, so when President Ferdinand “Bongbong” Marcos, Jr. banned them last year, it was a good move.

The next entry point of big money laundering in the country would be illicit trade in tobacco, oil, jewelry, and other consumer goods — with hundreds of billions of pesos yearly lost in foregone taxes. The government should crack down on these to avoid landing on the grey list again someday.

Recently, both the Bureau of Customs (BoC) and Bureau of Internal Revenue (BIR) issued separate but related statements on illicit trade. “BoC Chief Rubio vows heads will roll after discovery of attempted resale of seized cigarettes” (Feb. 22), and “Commissioner Lumagui orders nationwide destruction of P2.1B worth of illicit cigarettes” (Feb. 24). These statements were about the attempted resale of P270 million worth of BoC-seized contraband cigarettes from Capas, Tarlac, and P2.1 billion of BIR-seized illicit tobacco. These two incidents alone would need large-scale money laundering schemes before the funds could be happily enjoyed by the smugglers and criminal groups. The BoC and BIR are both under the DoF, so they must have seen the Finance department’s clear signal to avoid getting on the FATF grey list again.

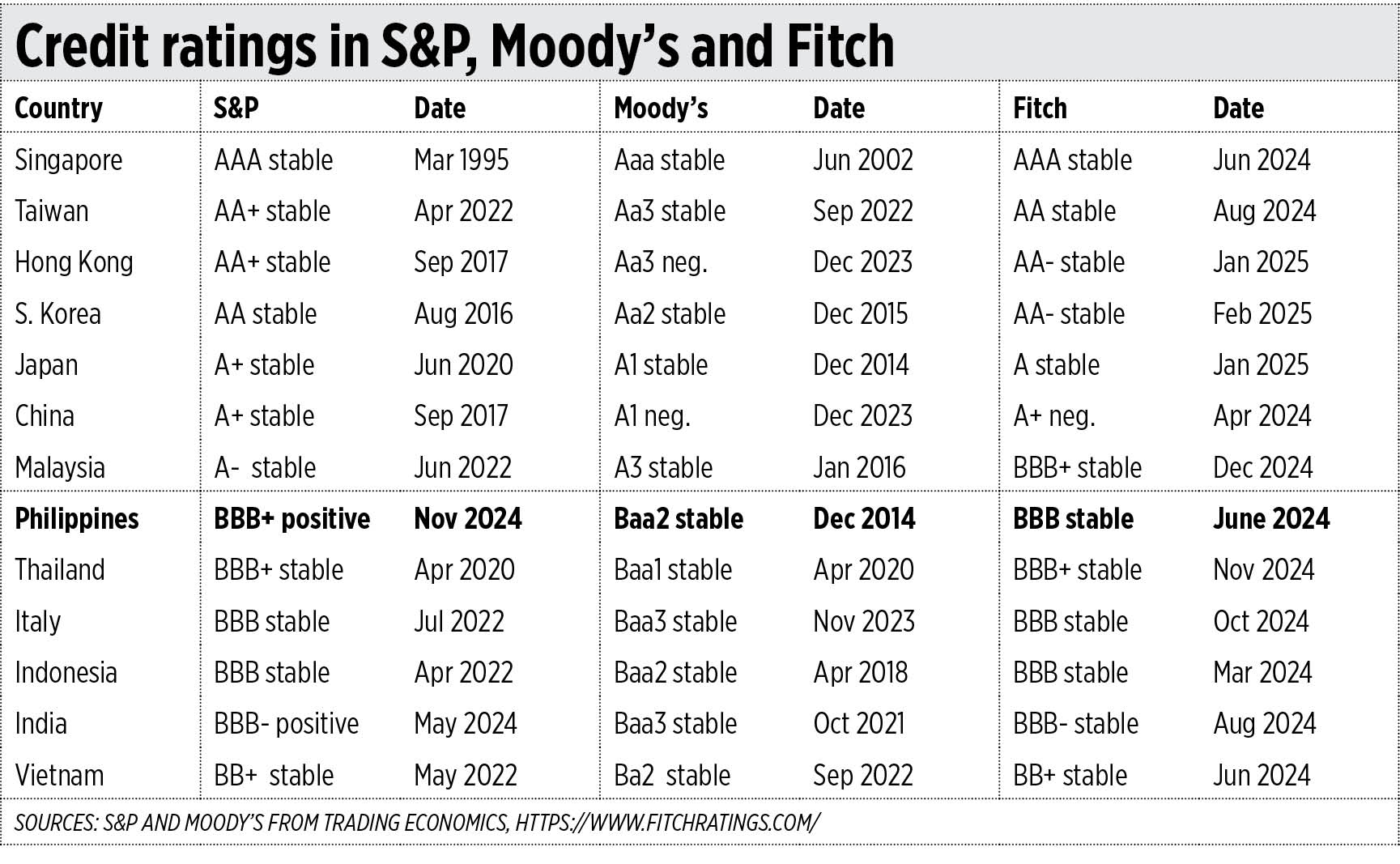

GETTING AN ‘A’The economic team has targeted making the Philippines get an “A” rating from any of the three big ratings agencies — Fitch, Moody’s, and S&P.

I reviewed the latest credit ratings of major East Asian economies. The Philippines is “BBB+ positive” according to S&P or just one step from “A,” is “Baa2 stable” with Moody’s or two steps away from “A3,” and “BBB stable” as per Fitch or two steps from “A-.”

And the Philippines has higher ratings than Thailand and even Italy under S&P. Surprisingly, Vietnam and India, which were the two fastest growing major economies in the world in 2023 and 2024, have lower credit ratings (see the table).

Budget Secretary Amenah F. Pangandaman said in a Viber message that “a Philippines ratings upgrade to ‘A’ from any of those three agencies would mean lower cost of borrowings for us to help finance the budget deficit and finance important social and infrastructure projects.”

This is a reiteration of her previous position as reported here, “Public-finance roadmap to help elevate PHL to ‘A’ credit rating — Budget dep’t” (BusinessWorld, Sept. 17, 2024).

Of course, I would prefer that we significantly cut expenditures, cut the yearly deficit, and hence cut the need for more borrowing whether at low or high interest rates. But in the absence of this scenario, low-cost borrowings via a ratings upgrade to “A” is preferable.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers. He is an international fellow of the Tholos Foundation.

{kind=link}