PHL monetary policy transmission remains ‘weak,’ AMRO says

MONETARY POLICY transmission in the Philippines remains “weak,” as seen in the muted movements in actual bank lending rates compared to the changes to the Bangko Sentral ng Pilipinas’ (BSP) policy rate, the ASEAN+3 Macro-economic Research Office (AMRO) said.

AMRO said in a special chapter of its annual consultation report for the Philippines released on Monday that the “weak pass-through” of BSP actions could reduce the impact of its monetary policy on the economy.

“In 2022-2023, Bangko Sentral ng Pilipinas tightened monetary policy forcefully by raising the policy interest rate by 450 basis points (bps) to fight off inflation. The magnitude of the increase was large compared with peer coun-tries such as Indonesia, Malaysia and Thailand. However, only half of the total change was reflected in the actual bank lending rate. Such a weak pass-through may hinder monetary policy effectiveness, given the bank-based nature of the Philippine financial system,” AMRO said.

“Effective monetary policy implementation requires a robust transmission of the policy rate to the interest rates in the broader economy.”

BSP Governor Eli M. Remolona, Jr. has said that the Philippines’ monetary transmission mechanism has long lags.

AMRO attributed the limited pass-through to “an abundance of low-cost funding and the lack of consumer credit data.”

“In the Philippines, since bank funding is the largest formal financing source for the private sector, the sensitivity of bank lending rates to the policy rate is central to monetary policy effectiveness,” AMRO said.

It noted that there are disconnects in several key policy transmission links.

“When the BSP adjusts its policy rate, known as the target reverse repurchase (RRP) rate, it should lead to corresponding changes in the short-term market interest rates at which banks lend or borrow funds from one another. These market interest rates influence asset prices, such as stock indices, bond yields and exchange rates. They also feed into bank funding costs, which are the basis for the pricing of bank deposit and lending rates. The bank rates and asset prices that consumers and firms face affect their demand for goods and services, and ultimately, domestic prices,” it said.

The first transmission link, which is from the policy rate to short-term market rates, has “worked well in some markets,” it noted.

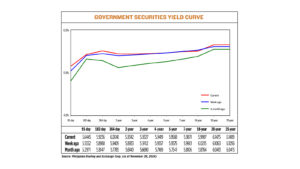

“Movements of the interbank call loan rate (IBCL), which is the overnight unsecured borrowing rate, and the short-term government bond yields have been well anchored to the policy rate since the establishment of the In-terest Rate Corridor (IRC) in 2016.”

The BSP adopted the interest rate corridor system in 2016 to help bring short-term market rates closer to its policy rate for better policy transmission.

“Before the IRC, insufficient liquidity absorption led the IBCL and one-year yields to trade significantly below the policy rate,” AMRO said. “However, after the IRC was put in place, the BSP introduced new liquidity ab-sorption tools such as the term deposit facility and the issuance of BSP securities, and these short-term market rates began moving more in line with the policy rate.”

However, the “interest rate in the foreign exchange swap market is more volatile and often trades below the policy rate,” it noted.

The Philippine Interbank Reference Rate (PHIREF), the implied peso interest rate derived from foreign currency (FX) swaps, depends “not only on domestic interest rate conditions but also US dollar funding conditions.”

“The PHIREF volatilities and deviations from the policy rate can dilute monetary policy signals, given that FX swaps remain the most active interbank market in the Philippines due to higher liquidity and more familiarity among participants compared with the repo market.”

AMRO added that there is also a disconnect between market rates and bank funding costs.

“Short-term market rates are only partially reflected in bank funding costs. Following the 450 bps increase in the policy rate and the comparable changes in many short-term market rates, the average funding costs of the banking system rose by less than 30% of that amount,” it said.

“The muted changes in bank funding costs are a result of the large low-cost deposit funding in the banking system,” it added, noting that in the BSP’s last tightening cycle, where the policy rate was hiked to a 17-year high, deposit rates only moved marginally.

“To be sure, from a bank’s perspective, a high NOW (negotiable order of withdrawal) and savings ratio supports profitability. However, from a monetary policy perspective, it limits the degree of policy transmission to bank rates and then to the economy overall,” AMRO said.

“The large surplus liquidity in the banking system also limits the rise in bank funding costs. The Philippine banking system has ample liquidity… Excess liquidity is also reflected by the loan-to-deposit (L/D) ratio, which is markedly lower than in ASEAN-4 peers The low L/D ratio shows that most banks have a sizable buffer of idle liquidity, and hence have no need to compete for deposits by using more attractive rates,” it added.

AMRO also noted the “constrained” linkage from bank funding costs to lending rates, with the pass-through differing depending on the loan type.

“After the policy rate was raised by 450 bps, the average effective lending rate rose by 224 bps, a pass-through of 50%. However, behind this average number, the degree of pass-through varies across loan types,” it said.

It noted that the degree of pass-through was strongest for corporate loans (64%), followed by small- and medium-sized enterprise loans (32%) and household loans (20%).

“Household loan rates are less sensitive to the policy rate because they are dominated by credit risk premiums. In simple terms, bank loan rates comprise bank funding costs plus the risk premium of the borrowers and the bank’s profit margins,” it said. “Based on AMRO’s interviews with banks, the credit risk component in household loan rates tends to be large, dwarfing any changes in funding costs that can be influenced by the policy rate.”

IMPROVING LINKAGESMoving forward, to strengthen the link between the BSP’s policy rate and bank lending rates, AMRO said the central bank should “continue to develop a liquid repo (repurchase) market to serve as the core interbank funding mar-ket with a stronger link to the domestic policy rate.”

The BSP and the Bankers Association of the Philippines have announced their plans to enhance the government securities repo market to boost the capital markets and improve asset pricing.

“Second, although stable bank funding is important for banking system resilience, the deposit market has room for more competition to enhance sensitivity to the policy rate,” AMRO said.

Increasing consumer awareness regarding alternative and higher-yielding savings and investment products would help monetary policy transmission, boost household savings and deepen the capital markets, it said.

Lastly, the quality and availability of household credit data should be improved to allow lenders to better assess credit risks and price loans, AMRO said.

“First, the data should be more complete, encompassing all financial footprints at bank and nonbank lenders. Second, the accuracy of the data must be improved. Third, alternative data such as payments to utility com-panies or online shopping platforms can be added to the credit profile, subject to appropriate data privacy and protection standards,” it said.

“Such improvements in the credit data will not only benefit policy rate transmission, but also provide opportunities to households with a good credit history to access finance at more reasonable costs.” — Luisa Maria Jacinta C. Jocson