Debt service, sustained growth, and the PDE alumni homecoming

During the post-State of the Nation Address (post-SONA) Philippine Economic Briefing (PEB) last week, July 25, at the Philippine International Convention Center, Finance Secretary Benjamin Diokno expressed continued optimism saying that “Higher economic activity and increased investments will bring us to even greater heights. The policy environment for foreign direct investments is the most open and liberal it has ever been.”

On the Maharlika Investment Fund (MIF), Secretary Diokno said “the MIF is expected to widen the fiscal space and reduce reliance on official development assistance (ODA) in funding big-ticket infrastructure projects.” Right on, Sir.

Budget Secretary Amenah Pangandaman was not there as she was presenting the National Expenditure Program (NEP) to President Marcos Jr. that will be submitted to Congress. Then the President flew to Kuala Lumpur for a state visit.

Budget Undersecretary Joselito Basilio took her place at the event and discussed the priority sectors under the FY 2024 proposed budget through the NEP that is anchored on the Philippine Development Plan (PDP) 2023-2028. Economic Planning Secretary Arsenio Balisacan highlighted social services spending in the PDP 2023-2029.

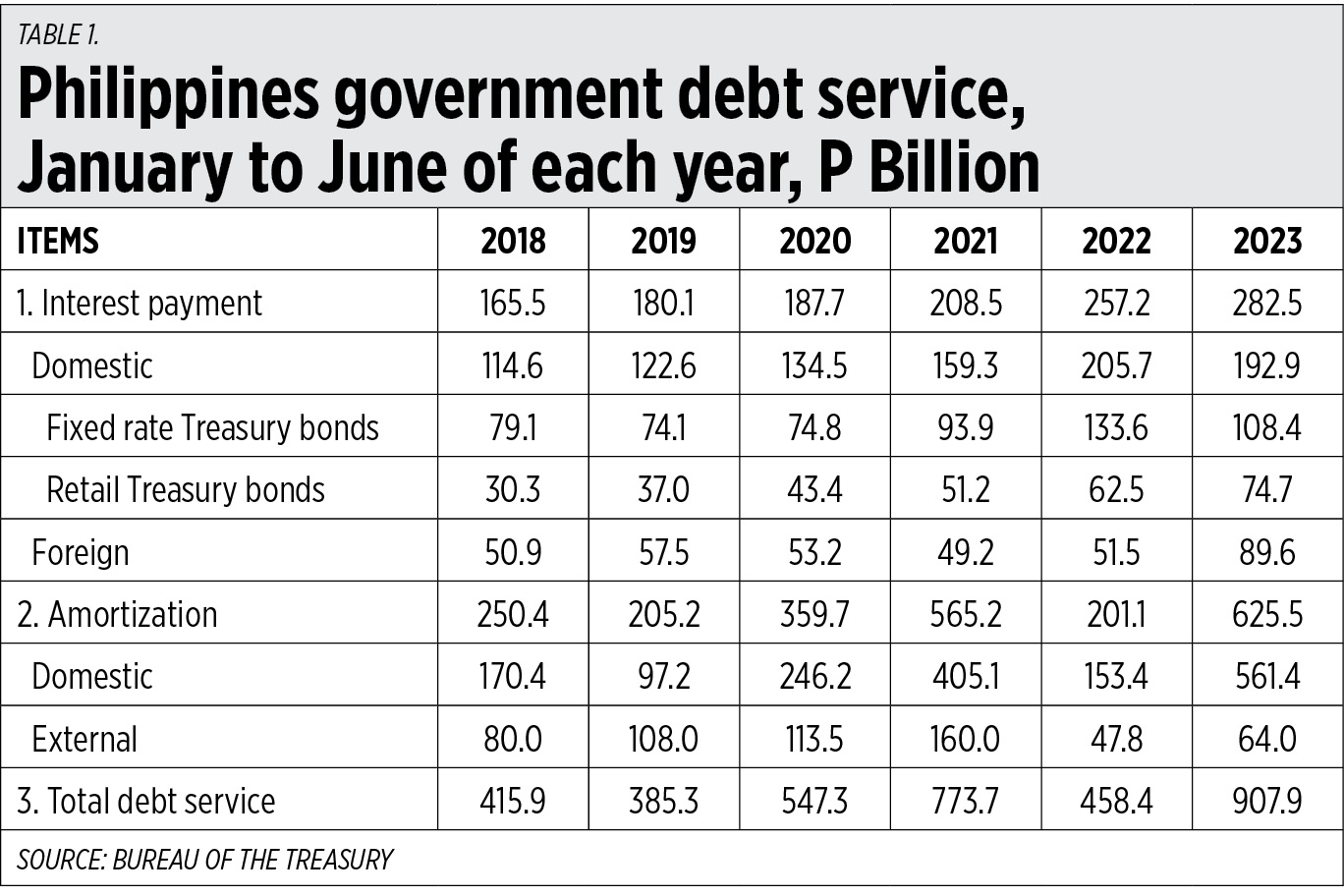

Also last week, the Bureau of the Treasury released the cash operations report including debt service for June 2023. Since the results of the first half (H1) of 2023 are already reported, I have compared the H1 numbers of previous years, 2018-2022. The numbers this year on debt servicing — payment in interest plus amortization for public debt contracted and accumulated for many years under previous administrations — are not good.

One — interest payment this year is already P283 billion, amortization is P626 billion, total debt service is P908 billion or approaching P1 trillion in H1 alone. This is not good.

Two — domestic debt constitutes a rising share of total debt service, especially in fixed rate and retail treasury bonds (see Table 1).

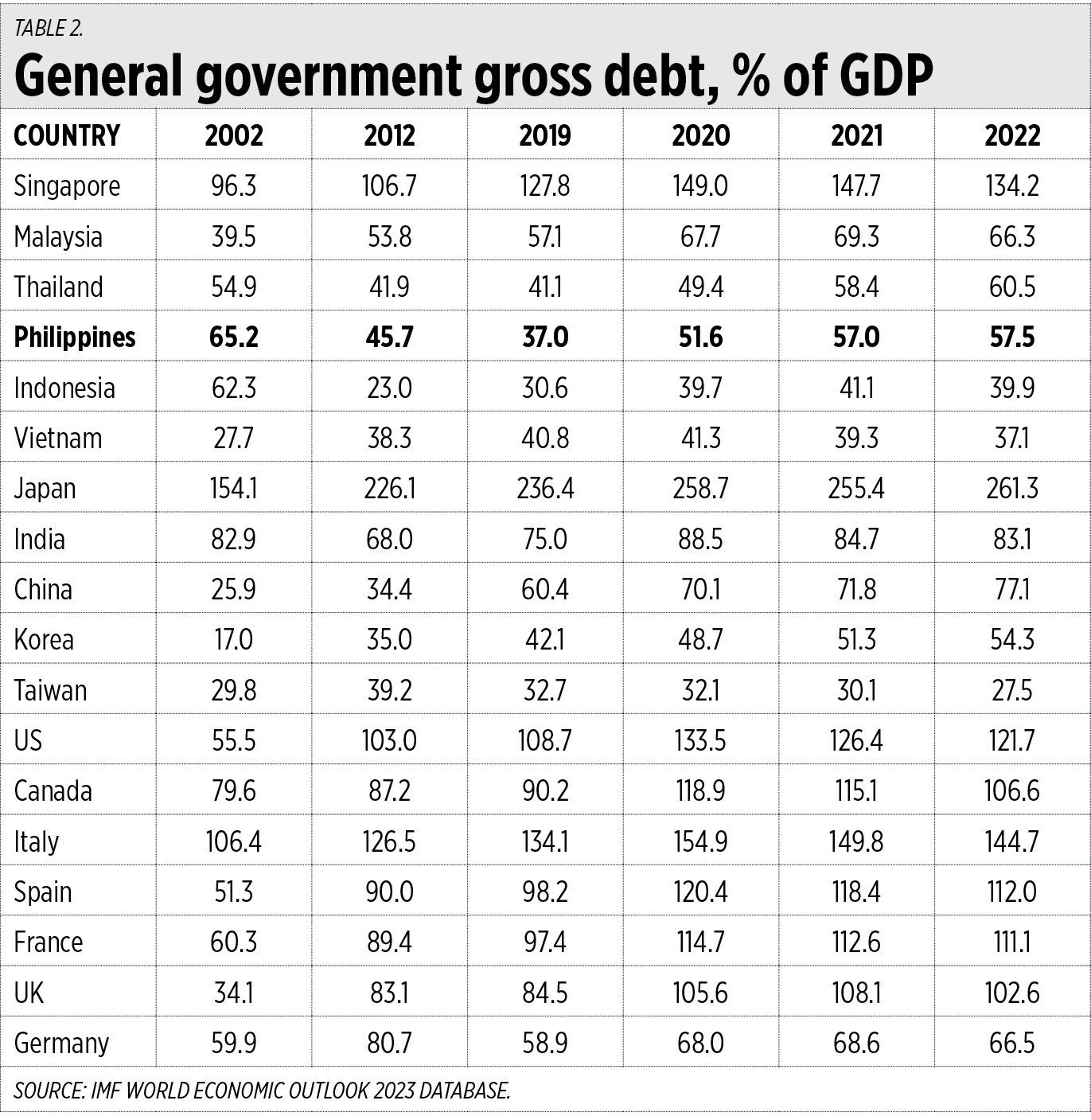

I checked the level of indebtedness of other countries. The gross debt/GDP ratio really jumped in the 2020-2021 lockdown dictatorship period, and began to flatline, or increase/decrease mildly in 2022. For the Philippines though, the jump was steep, from 37% in 2019 to 52% in 2020 then 57% in 2021. The lockdown dictatorship of the previous Duterte administration was really harsh compared to many countries, in Asia and around the world. Recall that Philippines GDP’ contracted 9.5% in 2020 — the worst in Asia, and the worst in Philippine economic history since after World War II.

Vietnam and Taiwan practically did not raise their indebtedness in 2020, they also managed to have GDP growth, not contraction, that year. For big countries in North America and Europe, all of them except Germany experienced debt/GDP ratios of 100% and above (see Table 2).

The above numbers show that lockdowns — shutting down of tax-paying businesses while expenditures remained high, then relying heavily on debt financing — is not good. It will never be good. Economic freedom — allowing people and companies to continue working and leaving healthcare to personal and civil society responsibility, not government lockdown irresponsibility — is the key to balancing economics and healthcare.

And the Maharlika Investment Fund? It is demonized by many individuals and groups concerned with public finance but who have little to zero (sound-of-silence) positions on military and uniformed personnel pension reform, a big public finance issue.

The Maharlika Fund should help finance big infrastructure and projects that were killed by politics (or subject to future political harassment) and hence, reduce fiscal pressure and need for borrowing. Since that new body has government presence and footprint, it can help thwart political harassment from local and National Government bureaucracies, as well as invite sovereign wealth funds from other countries to put their investments here as those projects have vetting and confidence by the MIF.

PDE ALUMNI HOMECOMINGMeanwhile, the Program in Development Economics (PDE) Alumni Association of the UP School of Economics (UPSE) will hold the PDE alumni homecoming on Aug. 19, 4 p.m., at the UPSE auditorium. Before the homecoming program, there will be “A Conversation with Finance and Budget Secretaries on Financing Sustained Growth.” The guest speakers will be Finance Secretary Diokno (PDE batch 7) and Budget Secretary Pangandaman (PDE batch 33).

These two officials are responsible for revenue generation and deficit borrowing and proposing the budget for the entire government to Congress, then manage its disbursement once enacted as appropriations act by Congress. They are key leaders in financing the very important goals of high sustained growth and sustained job creation while reducing the huge public debt accumulated by previous administrations.

PDE graduates from different batches, from the late 1960s to 2023, are encouraged to attend this very important lecture and meeting with their fellow alumni Cabinet Secretaries. This is a by-invitation event only, with some media and friends who are non-PDE alumni also invited to the “Conversation” before the homecoming program starts. Dinner will be served by the Philippine Center for Economic Development (PCED).

For the homecoming program, the PDE Alumni Association officers — including this writer — have solicited donations in kind from some corporations for raffles and give aways to participants. The following firms have expressed their willingness to give: San Miguel Corp., Robinsons Retail, Meralco, Astoria Hotels and Resorts, Nestlé Philippines, Gallerie Joaquin, Japan Tobacco, Inc., iOptions Ventures Corp., Philip Morris Fortune Tobacco Corp., and Alas Oplas & Co. CPAs. Thank you.

Thank you, Ferdie, Robina, Joe, Jeffrey, Arlene, Jack, Robert, Pidro, Noel, and my sister Marycris and their respective companies above. They are mostly my friends and fellow alumni of UPSE plus other friends and my sister.

Last month, this column produced a four-part series on Financing Sustained Growth: MUP pension reform (part 1, June 6), Fiscal discipline and Maharlika fund (part 2, June 13), Tax reforms (part 3, June 15), and NAIA privatization (part 4, June 27).

After the talks and “Conversation” with the two Secretaries, this column will resume another series on Financing Sustained Growth. Tune in, dear readers.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers.

{kind=link}

{kind=link}