Get real with inflation

Philippine annual inflation quickened to 6.9% in September, hitting its fastest pace in four years, driven mainly by high food and utility prices, according to the Philippine Statistics Authority (PSA). The 6.9% inflation growth rate is well outside the 2% to 4% target of the Bangko Sentral ng Pilipinas (BSP), which has so far raised rates by a total of 225 basis points this year to try and stem inflation.

“The Bangko Sentral is prepared to take further policy actions to bring inflation toward a target-consistent path over the medium term, consistent with its primary objective to promote price stability,” the BSP said in a statement. More rate hikes are expected at its November and December meetings (Reuters, Oct. 5, 2022).

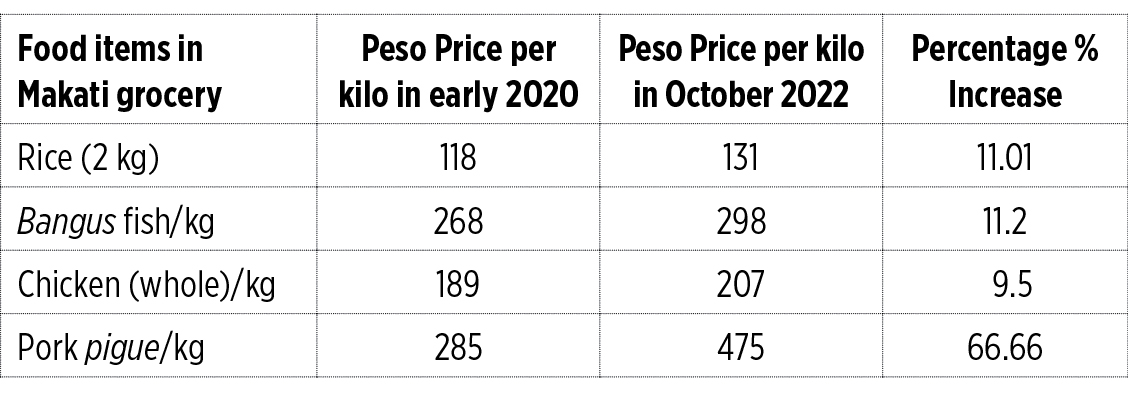

“I don’t know what you say about this ‘inflation’ thing,” the ordinary Pinay housewife might say. All she knows is that grocery prices have gone up in the two and a half years of the COVID pandemic, and prices are still going up. (Disclaimer: “housewife” is not a derogatory term for women, or wives, or stay at home persons, but used only to un-maliciously represent the ordinary consumer who is simply concerned about personal purchasing power.)

The price changes in the sample grocery food items in the table, plus the escalating prices of fuel and gas, electricity, water, and housing in the last 2-½ years may basically represent the layman’s most common perception of today’s inflation. The PSA, as with world economic measurements and statistics agencies surveys, meticulously derives inflation from what is called the Consumer Price Index (the CPI market basket), the weighted arithmetic mean of expenditures on 11 classes of consumer items purchased by households as a proportion to total expenditure.

The retail prices of food and non-alcoholic beverages are 38.96% and housing, water, electricity, and gas are 22.47% of the CPI market basket, while alcoholic beverages and tobacco, clothing and footwear, health, transport, communication, recreation, education, and restaurant and services contribute percentages of from 2% to 7% (only transport) to the representative market basket. The 2006 CPI series was the first in the CPI series that used the 1999 United Nations Classification of Individual Consumption According to Purpose (COICOP) in determining the commodity of the items and services included in the market basket (psa.gov.ph).

The inflation rate is the annual rate of change, or the year-on-year change of the CPI expressed in percent. Inflation is interpreted in terms of declining purchasing power of money. But note the “housewife’s” uncanny intuition and accurate grasp of the on-the-ground situation wherein inflation is experienced — in real time, and not in the lagged effects hampering meticulous econometrics from perhaps arbitrary statistics.

Compare what the PSA said, “for food index, it increased to 8.3% in September 2022, from 7.7% in the previous month.” So, the ordinary layman knows and feels inflation even before PSA has measured the 6.9% official inflation rate while pre-announcing the key rate upward-adjustments. Increased interest rates will push up borrowing (and therefore production costs) for businesses, specially the small-to-medium enterprises — which costs will be passed on to the consumers, which will then push more inflation coming from the debilitated purchasing power of money.

Cost-push inflation, the economists call it, but the jargon is itself confused, as frustrated demand from weakened purchasing power increases demand even more, and inflation raises evil laughter at its triumph in entrenching itself in adaptive expectations of consumers who resign themselves to the irreversibility of prices that have gone up and which will never again go down. “Sticky prices” is the cutesy name for this.

Likewise “sticky” are wages, which in times of inflation are insistently pushing for upward adjustment, for workers to keep up with rising living costs while the companies they work with are struggling to keep production costs down or lower — the price-wages spiral raises inflation some more.

Like the price of goods and services, and of wages which will never go back to what they were in the good old days, the foreign currency exchange rate is likewise affected by the cumulative effects of historical periodic inflations. External inflation comes with the movements (depreciation, for the less-developed economies) from proportional inter-country difference in nominal interest rates as countries wrestle with their own inflation problems. The “housewife” probably does not fully understand that the US Fed has been increasing its interest rates to tame internal inflation, but she intuitively knows that the Philippine Peso is nearing the exchange rate of P60 to $1, and her groceries and other shopping will cost more pesos because most of consumer goods and services are fully imported or of imported content. Government financial managers and planners are the ones to worry about the “balance of payments,” where the country is a net importer, using US dollars to pay suppliers and creditors for foreign loans and obligations.

But the exporters and the Overseas Filipino Workers (OFWs) are happy at the depreciation of the Philippine peso, as they now have almost 20% more pesos in exchange for their dollars. As of last year, OFW remittances hit a record-breaking $34 billion, which, according to the BSP, accounted for 8.9% of the country’s GDP. In July 2022 alone, money sent home by OFWs increased by 2.3% to $3.24 billion from $3 billion, the BSP said. Sad to say, but the bonanza from the peso depreciation for exporters and OFWs/dollar earners will not really help the payment of government’s foreign loans obligations, because payments will still be in dollars, at the same principal, terms, and interest rate as contracted — only costlier, in terms of more pesos needed for servicing.

And here is where we have to “get real” with this complicated experience called “inflation.” Although the terms CPI and inflation are often used interchangeably, the CPI only measures inflation as experienced by consumers — like the “housewife.” This economic label is “nominal/headline inflation,” based on the CPI, or a CPI without volatile food prices and fuel, etc., called “core inflation.” But inflation is not just about the erosion of purchasing power.

Inflation affects macroeconomics (the country’s and world economics); microeconomics (economics of the firm or business); and personal finance and economics. “Inflation,” as economists try to measure it, or as the consumer really feels it, hits all who spend and use money. Take, for example, interest rates: the real interest rate is the nominal (or stated) interest rate less the rate of inflation. For investments, the inflation rate will erode the value of an investment’s return by decreasing the rate of return. Case: if the rate of return for government securities bonds is 4% gross and about 2.8% net of taxes and brokers’ fees, and the inflation rate is 6.9%, then the real rate of return for the buyer (the common investor) will be 2.8% less inflation of 6.9%, or a (negative) -4.1%! That’s because the interest rate of 4% is adjusted downward by 6.9% to account for the unfortunate power of inflation to erode value!

Why naman?, poor Filipinos ask the government.

The government should concentrate on providing a more confident economic environment for the country, not by reactive monetary and fiscal solutions to what has already threatened the survival and sustenance of the people, but by judicious and non-political medium- and long-term economic plans and programs.

Amelia H. C. Ylagan is a doctor of Business Administration from the University of the Philippines.

{kind=link}