Here comes the Son

Iam pleased to share excerpts from our Globalsource Partners quarterly forecast report (May 31), the summary page, and the concluding political section. GSP (globalsourcepartners.com) is a subscriber supported network of independent analysts in emerging market countries providing macro, financial and political risks analysis and forecast based in New York. Christine Tang and I are their Philippine Advisers.

SUMMARY FORECASTThe Philippines just elected its first majority president since the return of democracy in 1986 and delivered a not typical “tandem vote” by choosing his running mate as well. The convincing mandate given to President-elect Ferdinand Marcos, Jr. and Vice-President-elect Sara Duterte resulted from a generally orderly election and subsequent quick count. The new administration will take office on June 30.

So far, the incoming administration has handed the business community what it wanted — a knowledgeable and experienced economic team, drawn from current and past administrations, that could hit the ground running. Despite looking like a gerontocracy, media interviews given by key members of the team reveal readiness to put into action learnings gleaned from decades of working in their respective fields.

Although there is palpable unease, including among foreign observers, with the rise of the son of the former dictator, we, like the rest of the business community, are opting to give the president-elect the benefit of the doubt especially during his honeymoon period. A challenging global environment awaits his administration with economic growth slowing down, commodity prices staying elevated, monetary policies and financial conditions tightening, neighbor China still under COVID-19 lockdown, and geopolitical tensions causing greater policy unpredictability.

Domestically, the president-elect will be facing difficult choices. At the macro level, fiscal policy is constrained by much higher public debt and continuing large budget deficits, monetary policy is constrained by rising inflation with interest rates on their way up, and the external sector is impaired by the deterioration in the terms of trade, increased reliance on food imports to manage domestic inflation and potential risk-off conditions aggravating capital outflows. He will also need to act quickly to avert power shortages over the medium-term.

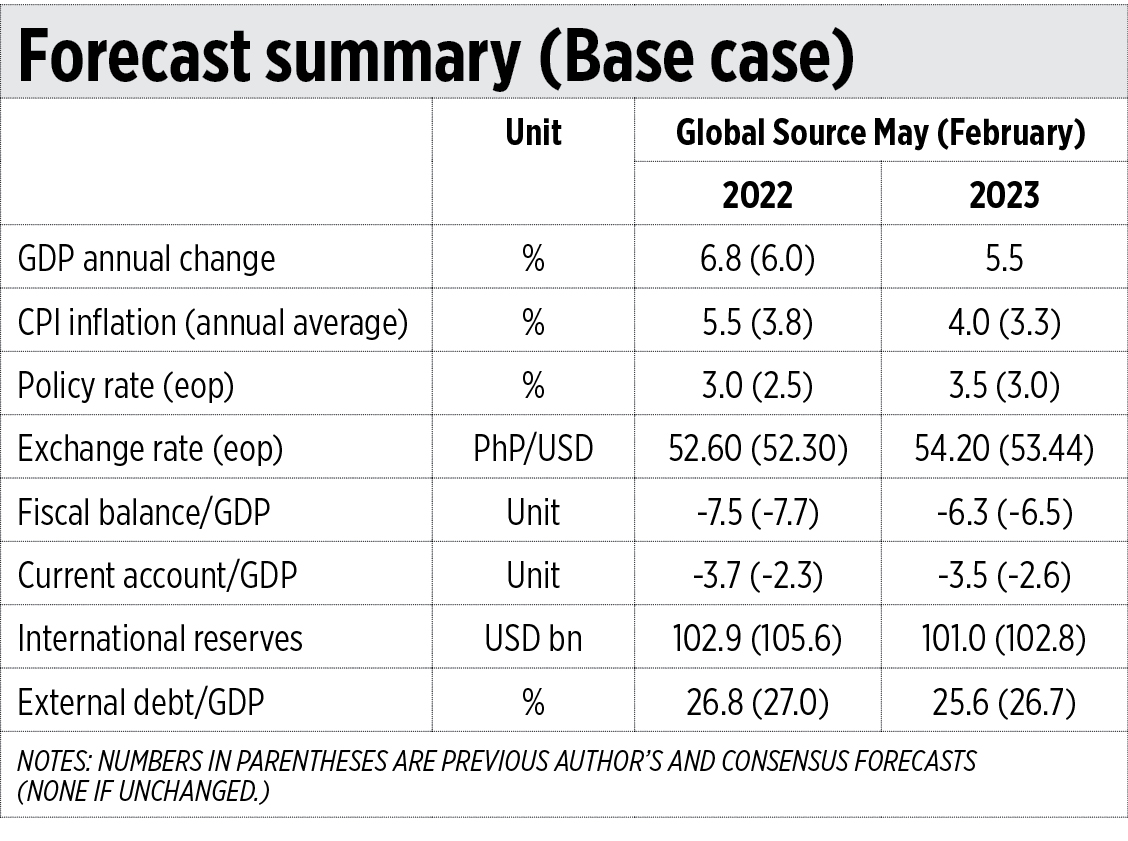

Although Q1 GDP growth was higher than expected, we think much of the surprise was due to election spending and unlikely to be sustained beyond 1H. However, the increased likelihood that COVID-19 has become endemic in the Philippines has raised our confidence in continuing freer mobility and gradual expansion of close-contact services, particularly tourism and in-person classes. We are thus raising our GDP forecast for 2022 from 6% to 6.8% but keeping our 2023 forecast at 5.5% pending clearer demonstration of the executive’s ability to build on and implement recent reforms, particularly in attracting foreign investments.

Downside risks are significant, emanating mainly from the many risks in the global environment, including US recession risk from much more aggressive Fed policy rate hikes and the impacts on highly indebted economies and emerging markets, possible escalation of the war in Ukraine and sanctions on Russia that could cause not just energy prices to soar anew but food shortages and more export bans, as well as a further slowdown in world growth due to the knock-on effects and China’s strict zero-COVID policy. Locally, downside risks include the continuing challenge of managing possible COVID-19 outbreaks, more rapid increases in inflation that de-anchors expectations and lead to more aggressive monetary tightening, and failure to maintain financial market confidence in the new administration’s commitment to macroeconomic stability in general and fiscal sustainability in particular.

Any upsides to enable the economy to sustain growth above 6% will hinge on the new administration’s ability to raise market confidence in its managerial ability and economic program (including broadening the base of economic growth), as well as a less tumultuous global environment that makes cross-border investment decisions possible. In this regard, recently legislated freer foreign investment rules can help attract foreign capital.

POLITICS: WHO HAS THE PRESIDENT’S EAR?He may look, talk and even share his father’s name but by all accounts, President-elect Ferdinand Marcos, Jr. is not his father, the strongman who ruled the Philippines for 20 years until his ouster in 1986.

For many, this is both good and bad: good, because he does not have the drive to become the autocrat that his father was; bad, because he does not have the vision to catapult his presidency to the heights afforded by his majority electoral win. In fact, the most worrisome political risk we hear now is that his may be a feckless presidency marked by indecisiveness and unresponsive leadership…

For longtime observers of policy making in the Philippines, it does not really matter who occupies the presidential palace and what his background and temperament are, as long as he knows how to delegate. President Duterte provides a radical example, practically giving his finance secretary, Carlos Dominguez, full control on the executive’s economic policy. His being the head of the economic team as finance secretary was greatly facilitated by the full trust of and access to the president, a relationship developed as early as primary school…

…. Many, ourselves included, think that Mr. Marcos could not have chosen a better economic team with the qualifications and experience that could hit the ground running during these challenging times. On the other hand, some of the members of this team must still remember their time in the Estrada government in the late 1990s, Mr. Diokno included who was then budget secretary, when the good policies framed by a first-rate economic team could not withstand the harm devised by an informal rent-seeking “midnight” cabinet.

For now, we can only give Mr. Marcos the benefit of the doubt that goes with his honeymoon period and trust in the experience and political instincts of his economic team. There are many challenging decisions on the economic policy front in the near term, including clarifying the President-elect’s campaign statements supporting direct government intervention in the rice and oil markets, that will reveal who has the president-elect’s ear.

Romeo L. Bernardo was finance undersecretary from 1990-96. He is a trustee/director of the Foundation for Economic Freedom, Management Association of the Philippines, and FINEX Foundation.

{kind=link}