Multilaterals list imperatives for PHL to sustain momentum

CONTINUED fiscal consolidation, implementation of reforms to boost private sector competition, and more investments in human capital are crucial if the Philippines wants to continue its strong growth momentum, according to multilateral lenders.

World Bank Country Director for Brunei, Malaysia, Philippines and Thailand Ndiamé Diop said there are three key areas the Philippines could focus on to ensure growth remains robust, and prosperity is spread across the population.

“It will be really important to further enable private investment and innovation to keep growth… Second is to double down on investment in human capital. Third is to bridge the digital divide and invest in adapting and integrating climate change,” he said at BusinessWorld Forecast 2024 economic forum on Wednesday.

Asian Development Bank (ADB) Country Director for the Philippines Pavit Ramachandran said these “imperatives” will be able to drive near-term development and support the Philippine growth outlook.

“It’s important that this growth momentum can be harnessed and enhanced in a way that really brings good opportunities for the private sector. I think you’ve got to have more of the private sector driving and serving as the engine of growth,” he said at the same forum.

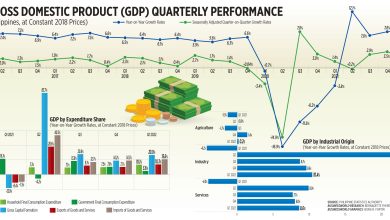

Economic managers are targeting 6-7% gross domestic product (GDP) growth for this year and 6.5-8% in 2024.

The World Bank gave a 5.6% GDP forecast for the Philippines this year and 5.8% for 2024. The ADB, on the other hand, expects the Philippine economy to grow by 5.7% this year and by 6.2% in 2024.

Mr. Diop said continuing orderly fiscal consolidation will enhance private investment and innovation in the Philippines, as this affects investor and trade sentiment.

The government is aiming to bring its debt-to-GDP ratio to below 60% by 2025 and the deficit-to-GDP to 3% by 2028.

Mr. Diop also said it is crucial to ensure that recent economic reforms to increase market competition such as the amended Public Service Act are fully implemented.

“Competition is really critical in the Philippines. If you look at many markets, limited competition is one of the reasons why prices are high. So, these reforms are really critical and if they’re fully implemented, they will really support the competitiveness of the economy,” he said.

Under the new law, telecommunications, domestic shipping, railways and subways, airlines, expressways and tollways, and airports were no longer subjected to the 40% foreign ownership cap under the Constitution.

Meanwhile, Mr. Ramachandran said the Philippines still has a lot of potential to attract more foreign direct investments.

Closing the physical infrastructure gap in the Philippines will also allow for faster transport mobility, facilitate access to opportunities, reduce travel costs, and boost productivity in the economy, Mr. Diop said.

He also noted that continued investment in upskilling the Philippine workforce will help sustain the economy’s growth momentum.

“Effective safety nets remain crucial in these times of high prices and hardship coming out of the pandemic. So, it’s really important to strengthen the system and focus on food security and improve existing social protection programs,” he said.

Mr. Diop said the Philippines needs to invest more in education and improve the quality of learning.

Meanwhile, International Monetary Fund (IMF) Representative to the Philippines Ragnar Gudmundsson said the government’s infrastructure program, opening up sectors to foreign investments, and private sector participation should help realize a growth potential of about 6.5% over the medium term.

“Boosting the country’s growth potential requires sustained efforts to raise productivity by reducing infrastructure and education gaps while promoting foreign investment,” Mr. Gudmundsson said.

“Sustaining significant growth gains over the past few decades and reaping the benefits of the demographic dividend will depend on further investments to diversify exports, promote the acquisition of new skills, and enhance connectivity across the archipelago,” he said.

According to the IMF, efforts to exit the Financial Action Task Force’s (FATF) “gray list” should be ramped up to reassure foreign investors and reduce financial transaction risks.

Since June 2021, the Philippines has been included in the global “dirty money” watchdog’s gray list of countries subjected to increased monitoring to prove its progress against money laundering and terrorist financing.

In its latest assessment in October, the FATF said the Philippines should continue to work on implementing action plans to address strategic deficiencies. — Keisha B. Ta-asan