On oil economics and Philippines vital statistics

On April 1, Israel bombed the Iran embassy annex building in Syria. Last Saturday, April 13, Iran sent hundreds of drones and cruise missiles to Israel. Since April 14, the world has been waiting to see if a large-scale counterattack by Israel would happen or not. As of this writing, there has been none; de-escalation of the conflict is good for the world.

OIL ECONOMICS: SUPPLY, DEMAND AND PRICESWorld oil prices did not jump up high after the exchange of bombs and missiles between the two countries. WTI crude went from $82/barrel in end-March to $87 on April 5 and $85 as of April 17. Dubai crude was $84/barrel in end-March and went up to $91 on April 5 and $90 as of April 17.

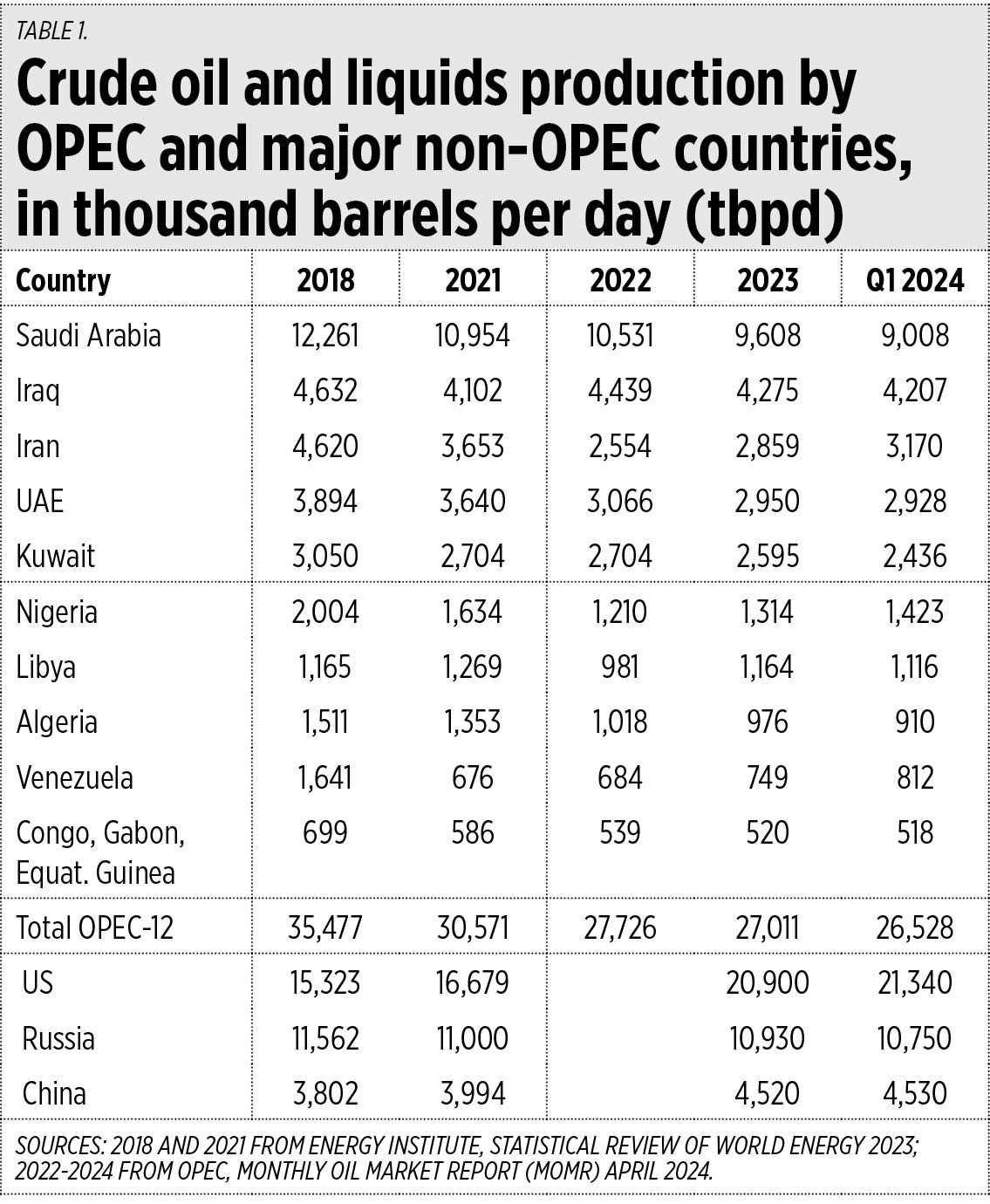

Iran is the third largest oil producer among the 12-members Organization of Petroleum Exporting Countries (OPEC). Its oil output was 3.2 million barrels per day (mbpd) in the first quarter of 2024. But a major war between Israel and Iran will affect not only Iranian oil output and exports but also those of the neighboring countries like Iraq, Kuwait, Saudi Arabia, and the United Arab Emirates (see Table 1).

The US is the largest oil producer and largest oil consumer in the world. In 2023, its total liquids output was 20.9 mbpd but its consumption was 20.6 mbpd. Not all oil is the same so US refineries still import a lot of oil from the Middle East, Africa, and South America with different qualities from US crude oil to produce the desired gasoline and petrochemical products.

Russia is the world’s second largest oil producer. In 2023 it produced 10.93 mbpd while its consumption was only 3.84 mbpd, giving it a surplus of 7.1 mbpd for exports, most of it going to China and India.

China is the fourth largest oil producer (Saudi Arabia is third) but it is the second largest oil consumer after the US. In 2023, China’s oil output was 4.52 mbpd while its consumption was 16.22 mbpd so to cover its deficit of 11.7 mbpd, it buys mostly from Russia, Iran, and Saudi Arabia.

Total global oil demand was 102.21 mbpd in 2023 and is projected to rise to 104.46 mbpd in 2024 and 106.31 mbpd in 2025 (data from OPEC). The bulk of rising global oil demand will be supplied by major oil exporters Russia, Saudi Arabia, and the other OPEC member-countries.

There are three main lessons to draw from current global oil economics.

One, global oil demand keeps rising despite all the demonization against oil and fossil fuels.

Two, de-escalation of the Middle East conflict, especially between Israel and Iran plus its allies in Yemen (Houthis), Lebanon (Hezbollah), Syria and Iraq (Shi’ite militias), and Palestine (Hamas), is very important.

Three, since all major military hot spots in the world have US involvement — Ukraine, Iraq and Syria, Israel-Iran, Taiwan, the South China Sea, etc. — the US should learn to step back from too much interventionism, allow disputing countries to talk to each other and resolve conflicts as peacefully as possible and help stabilize global energy markets.

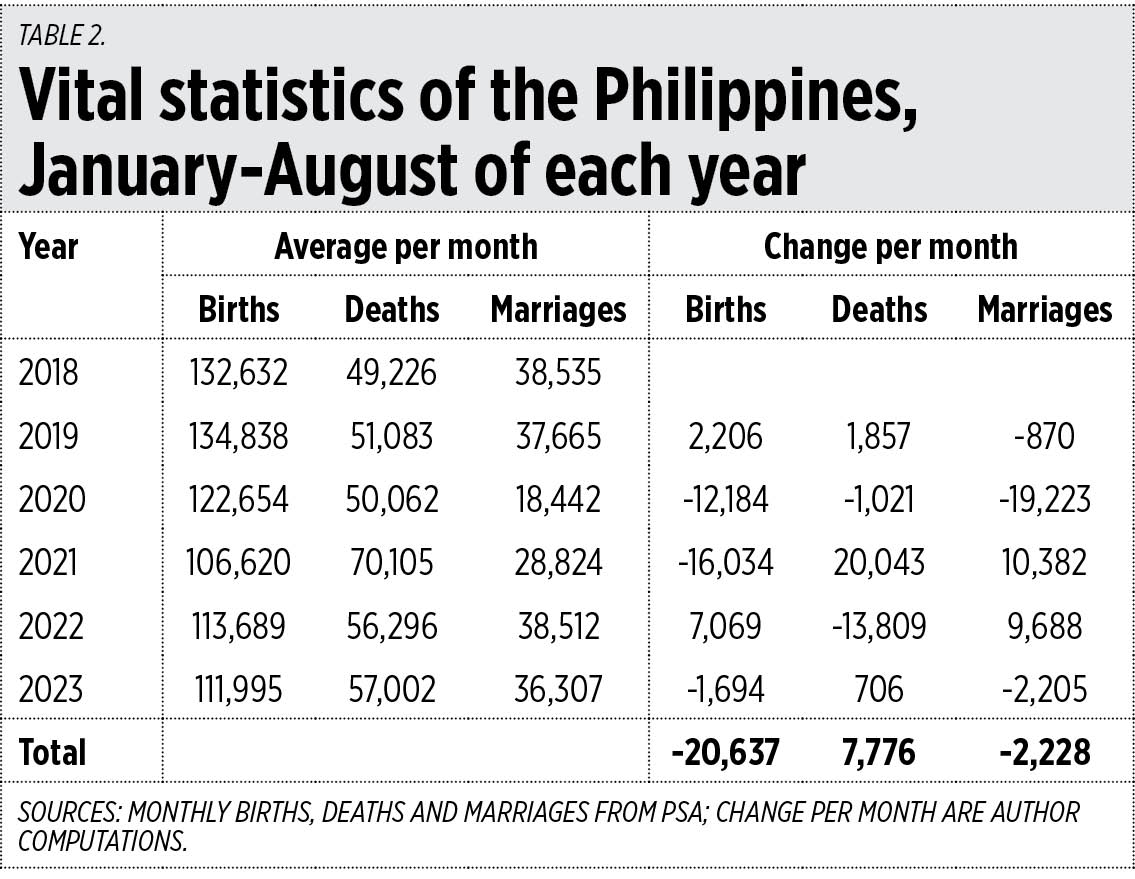

PHILIPPINES VITAL STATISTICSLast week, the Philippine Statistics Authority (PSA) released the monthly update of the country’s demographics and mortality statistics for 2023. I summed up the total for January to August and compared it with data for the same period in preceding years. The results are not exactly good.

One, the number of births has been falling since the imposition of lockdown dictatorship in 2020-2021 and mandatory COVID vaccination in 2021-2022.

Two, there were no excess deaths in 2020 over 2019 despite the high number of reported COVID cases, but there was a high number of excess deaths in 2021 (when mass vaccination was done in March 2021 onwards) compared to 2020 and 2019. There were 20,000/month excess deaths in 2021.

Three, the number of marriages significantly declined in 2020-2021 during lockdown. This recovered in 2022, going up to 2018’s level, then declined again in 2023 (see Table 2).

The COVID vaccines, being experimental with no long-term studies on their effect on heart conditions, fertility, and other health indicators, could be a major factor for the rise in excess deaths in 2021 and the decline in births until 2023 and possibly until today.

Economic scarring like the -9.5% GDP performance in 2020 (the worst in Asia that year, the worst in Philippine economic records since post World War 2), very high unemployment numbers and increase in business bankruptcies, and now an emerging demographic problem of declining births — these are the major damage caused by the lockdown dictatorship and mandatory vaccination.

Philippines government, business, and civil society leaders should keep this in mind: that curtailing economic freedom, disrespecting natural immunity from the virus and believing only in so-called vax immunity, are a sure formula for economic underdevelopment and demographic distortion.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers. He is an international fellow of the Tholos Foundation.

{kind=link}

{kind=link}